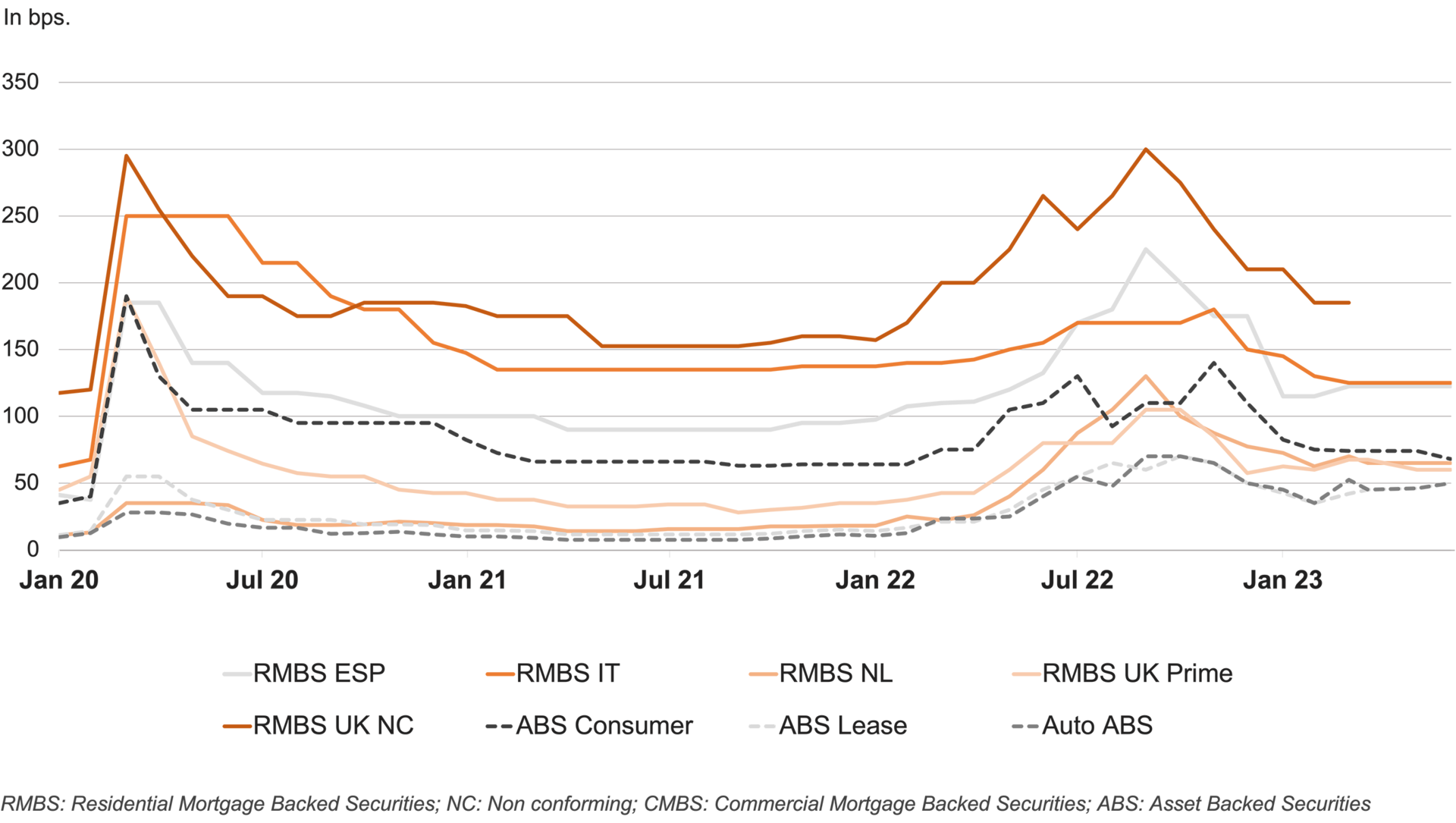

Public securitisations in Europe are regularly issued as floating rate bonds, and the yield is measured as a spread in basis points above a reference interest rate (usually 1 month Euribor). The charts below show how spreads depend, among other things, on the macroeconomic environment, and how the biggest changes are reflected in the period of the euro debt crisis in 2013 and the start of the corona pandemic. In terms of short-term developments, we can see that the renewed widening of spreads triggered by the Ukraine war was reversed at the beginning of 2023. Overall, the auto ABS asset class, which is particularly important for the German market, has proven to be the most stable.