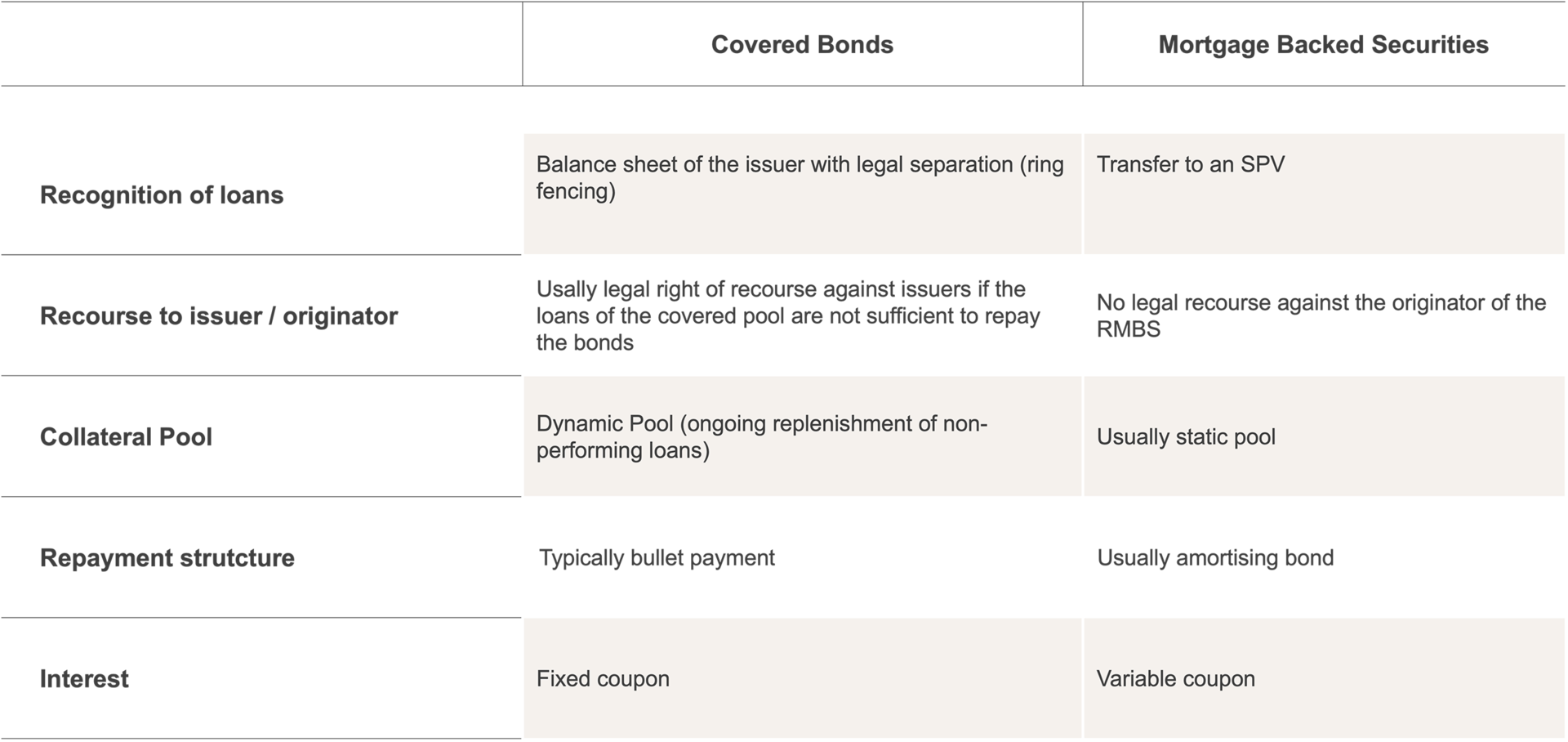

Stringent requirements are also placed on the quality of the receivables pool for covered bonds, and issuers must meet these requirements at all times. In Germany, the Federal Financial Supervisory Authority (BaFin) and an external trustee, as independent control body, are responsible for monitoring the quality of the receivables pool. In terms of their asset-backed structure, covered bonds are similar to securitisations. In the case of ABCP securitisations in particular, a form of double collateralisation is commonly employed in order to prevent possible liquidity risks. In these securitisations, a bank with a first-class credit rating often provides a liquidity line (sponsor). A special purpose vehicle can draw on this in the event of temporary payment bottlenecks. If the sponsor becomes insolvent, this form of double collateralisation of securitisations might be more beneficial for the investor than covered bonds. This is because the underlyings of securitisations with shorter maturities of less than one year, such as ABCP, generally amortise more quickly than the receivables in a cover pool comprising Pfandbriefe.

Compared to securitisations, covered bonds have the advantage of dual recourse, i.e. the liability of the issuing bank in addition to the collateral pool. On the other hand, securitisations offer the advantage of lower asset encumbrance, i.e. fewer assets needed to secure liabilities, as well as uniform regulation throughout Europe and significantly greater transparency.