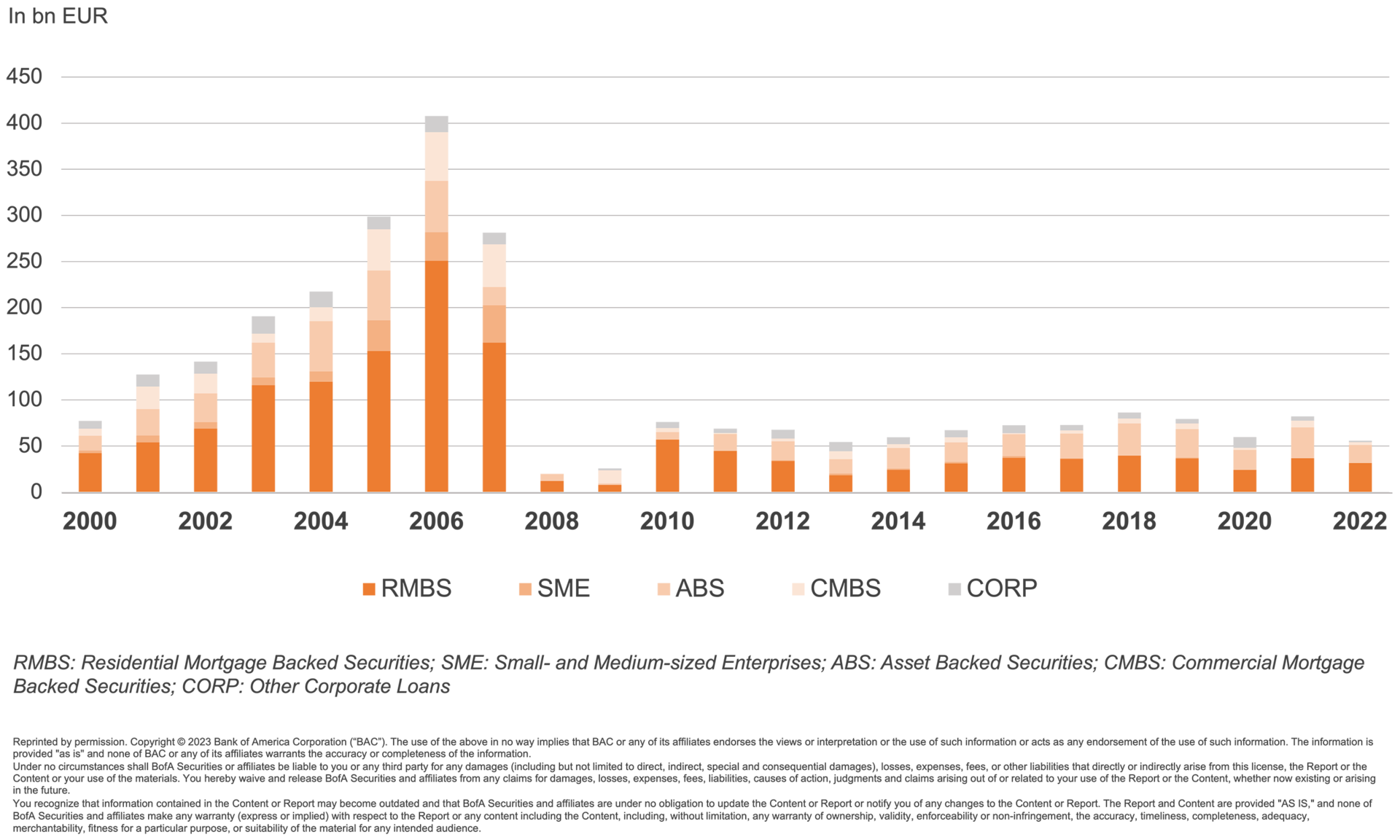

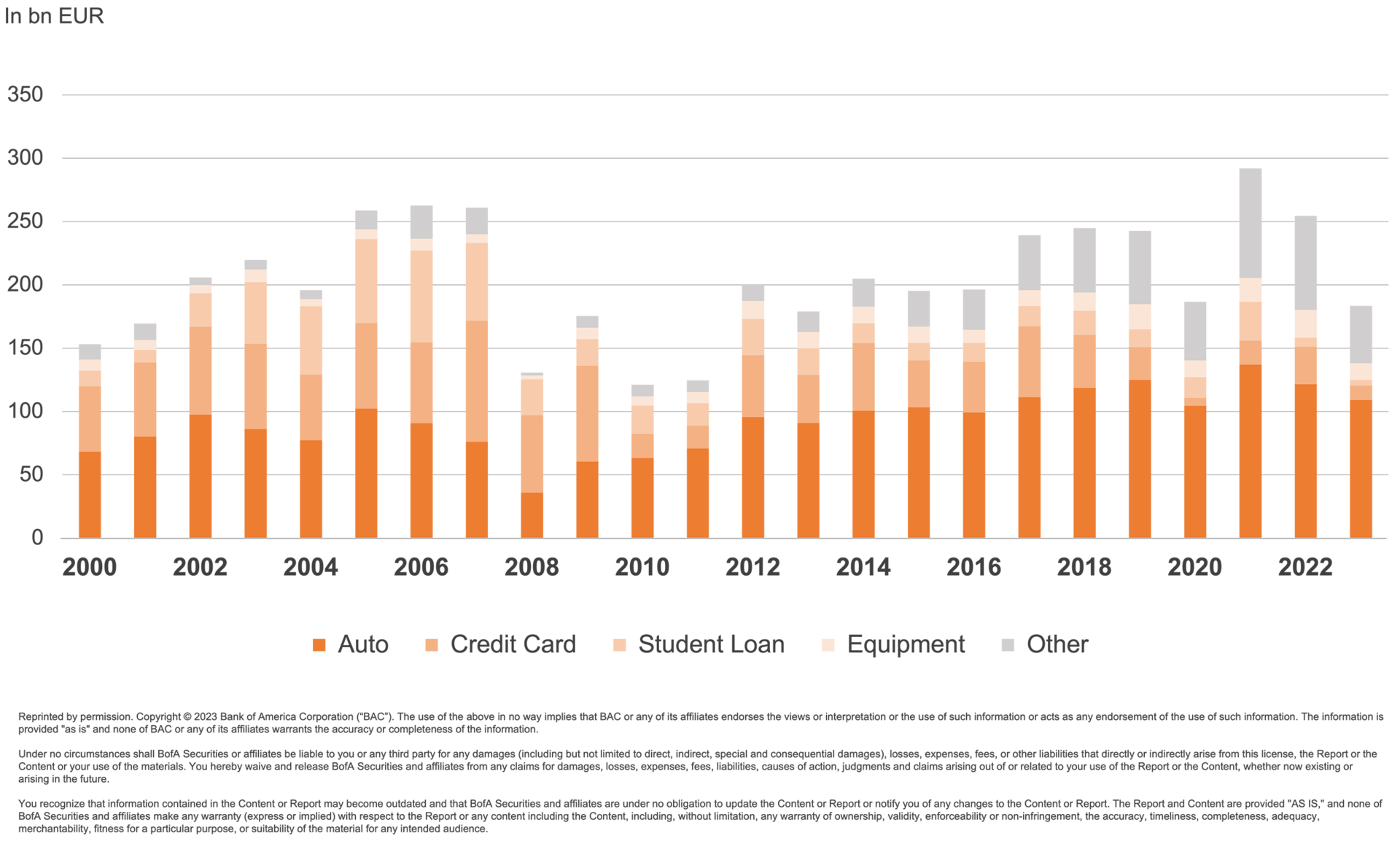

Since the global financial crisis in 2008, securitisation has often been viewed critically in the public sphere. However, this broad perception is at variance with the positive and proven performance of European securitisations –- before, during and after the financial crisis. In contrast to the USA, Australia and China, the securitisation market in Europe has hardly grown since the global financial crisis.