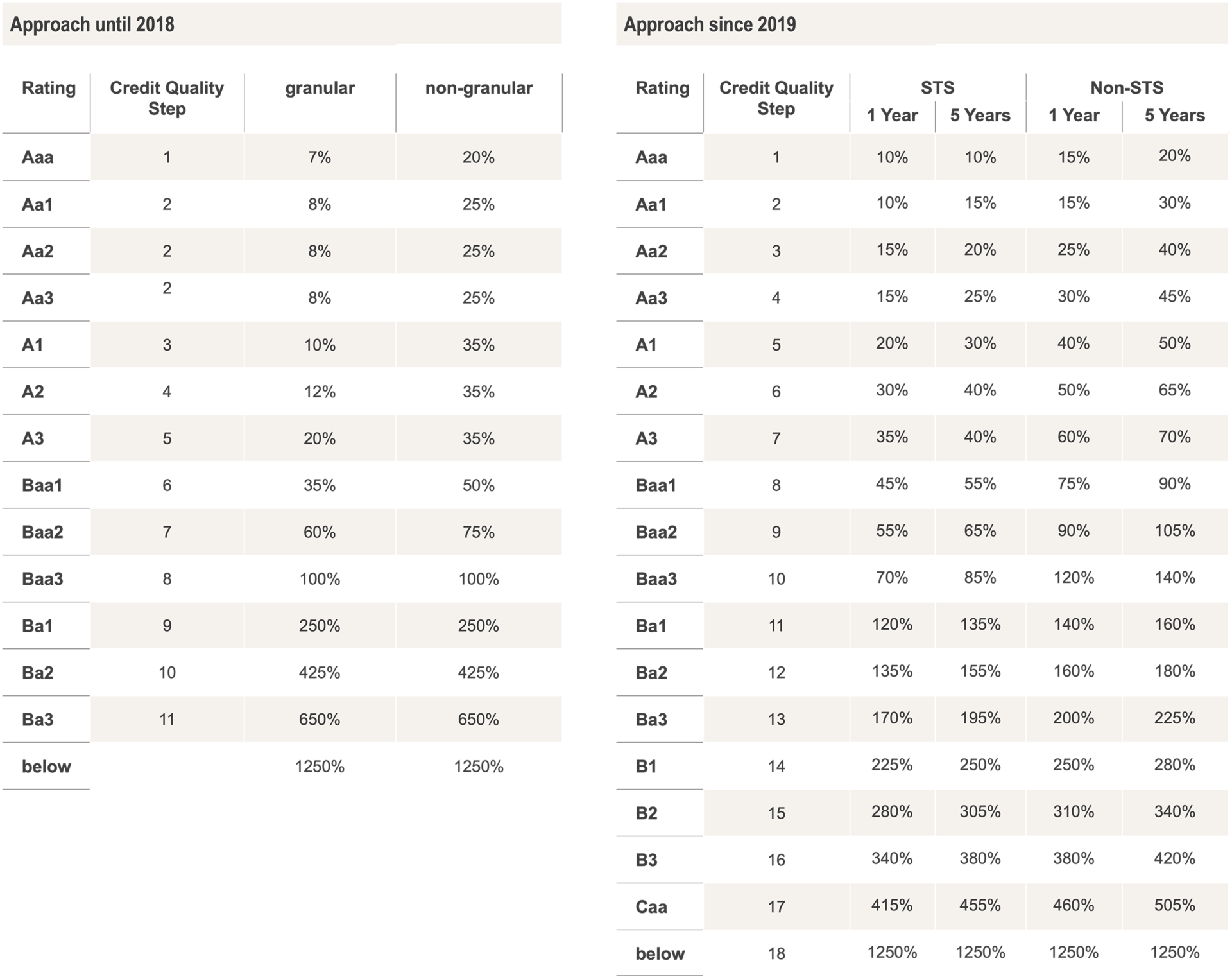

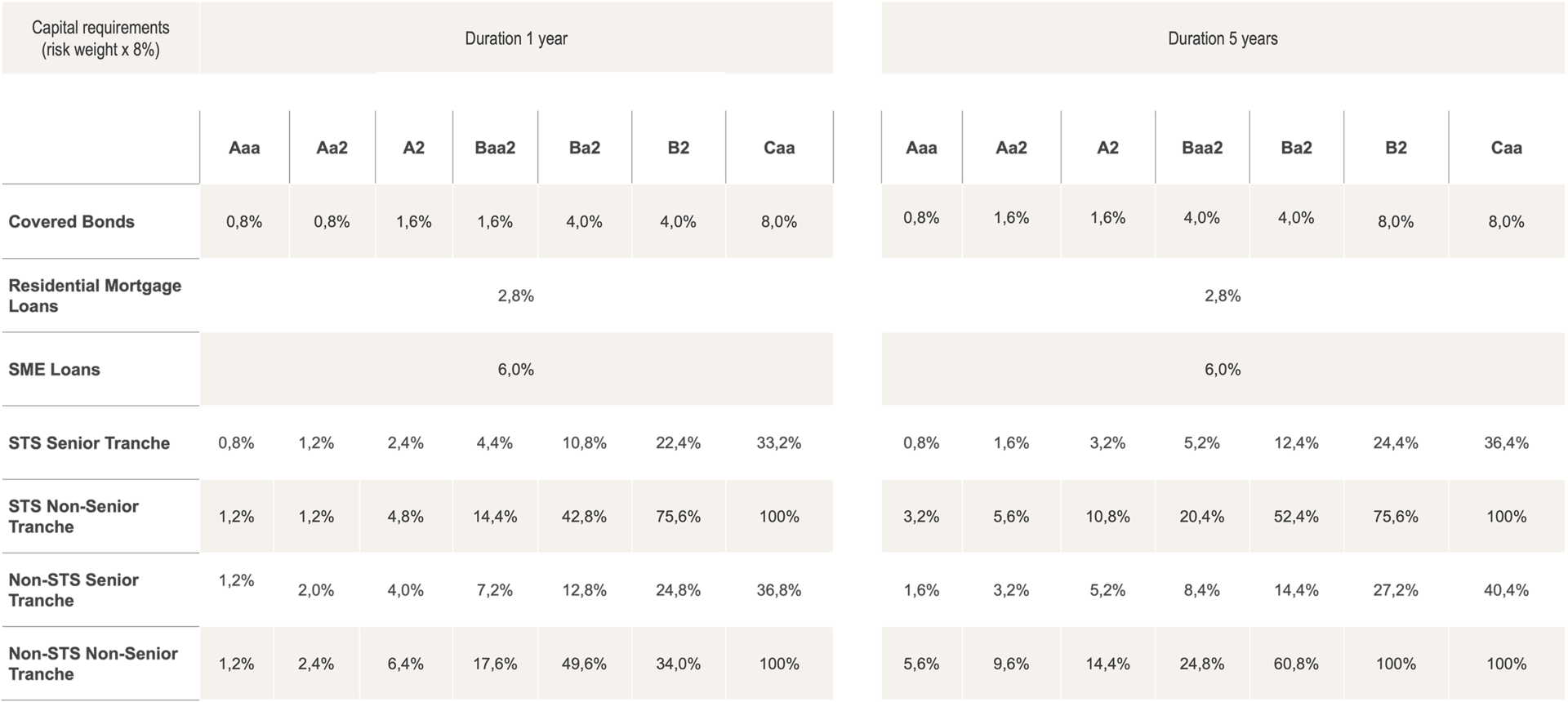

It can be clearly seen that, in relative terms, the capital requirements for securitisations are not adequate, especially as the transparency requirements for securitisations are significantly higher than for other financial instruments (loan-by-loan data vs., for example, aggregated pool data for covered bonds). Furthermore, the due diligence requirements for securitisations are also the highest by comparison. The imbalance in capital requirements despite comparable or even lower risks puts securitisation at a disadvantage compared with other financial instruments in the market.